For 5% additional off on first year premium Please contact +917981002025/+918297486673

Choosing Right ULIP's from HDFC life

Unleashing Your Investment Potential with HDFC Life ULIPs

Sai Teja

1/13/20254 min read

Unleashing Your Investment Potential with HDFC Life ULIPs

In today's dynamic financial landscape, you need investment solutions that offer both growth potential and security. HDFC Life's Unit Linked Insurance Plans (ULIPs) provide a powerful blend of investment and insurance, enabling you to build wealth while safeguarding your loved ones. Let's explore some of the key offerings:

1. HDFC Life Sampoorn Nivesh:

Benefits: This ULIP offers a comprehensive investment solution with a wide range of market-linked funds to choose from. You have the flexibility to customize your investment strategy based on your risk appetite and financial goals.

Why take it: Ideal for long-term wealth creation with the flexibility to manage your investments according to market trends and your changing financial needs.

2. HDFC Life Click 2 Invest ULIP:

Benefits: This plan combines the security of life insurance with the potential for higher returns through market-linked investments. It offers a diverse range of investment options and flexible premium payment options, making it suitable for those seeking a balance between risk and reward.

Why take it: A smart choice for those looking to build long-term wealth while maintaining a safety net for their loved ones.

3. HDFC Life Click 2 Wealth:

Benefits: Designed for those who prioritize wealth creation and financial security. This ULIP combines life cover with investment options, allowing you to invest in a diversified portfolio of funds and potentially achieve your ambitious financial goals.

Why take it: Ideal for individuals with a strong desire to build wealth and secure their financial future.

Key Features of HDFC Life ULIPs:

Flexibility: Choose from a wide range of investment options based on your risk tolerance and financial goals. You can select from equity funds, debt funds, balanced funds, and more, allowing you to tailor your portfolio to your investment objectives.

Transparency: Access to regular fund performance updates and portfolio information through online portals and customer service channels. This allows you to track the progress of your investments and make informed decisions.

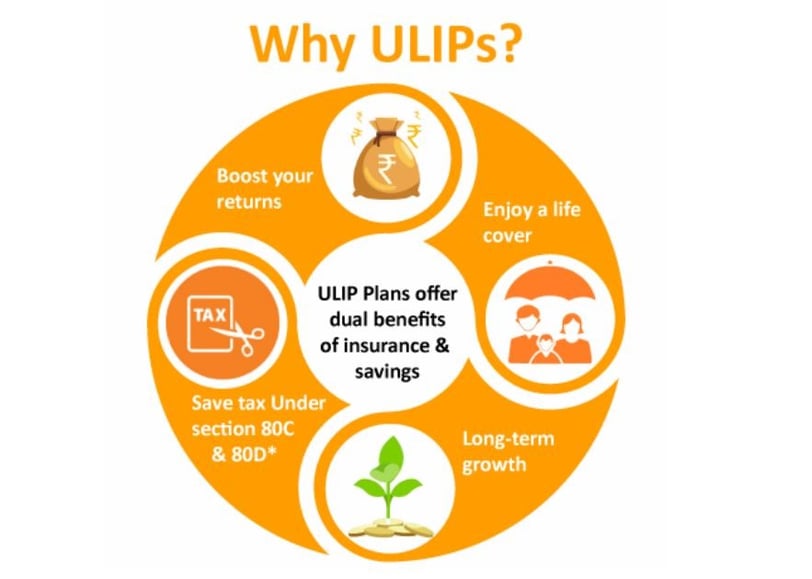

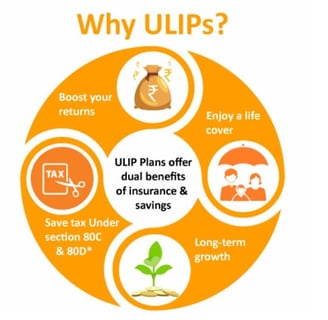

Tax Benefits: Potential tax benefits on premiums and returns under section 80C and 10D, subject to applicable tax laws. This can help you maximize your returns and minimize your tax liability.

Life Cover: Provides financial security to your loved ones in case of unforeseen events. This ensures that your family is financially protected even in your absence.

Flexibility in Premium Payments: Choose from various premium payment options, such as regular monthly payments, single lump sum payments, or limited premium payments, to suit your budget and financial situation.

Partial Withdrawals: Some ULIPs allow you to make partial withdrawals from your fund value, subject to certain terms and conditions. This can provide you with liquidity when you need it.

Choosing the Right ULIP:

Selecting the right ULIP depends on your individual needs, financial goals, and investment horizon. Consider factors such as:

Your age and risk tolerance: Younger investors may be more comfortable taking on higher risks, while older investors may prefer more conservative investment options.

Your financial goals: Are you saving for retirement, your child's education, or a down payment on a house? Your investment strategy will vary depending on your goals.

Your investment horizon: How long do you plan to invest your money? Longer investment horizons generally allow for higher risk investments.

Consulting with a qualified financial advisor can help you assess your risk profile, understand your financial goals, and select the ULIP that best suits your needs.

Remember: ULIPs involve market-linked investments and are subject to market risks. The value of your investments may go up or down depending on the performance of the underlying funds. Please read the product brochure carefully before making any investment decisions.

It's crucial to understand these charges to make informed investment decisions. Here are some of the common charges associated with ULIPs:

1. Premium Allocation Charge:(HDFC will payback these charges during policy terms)

What it is: A percentage of your premium is deducted as a charge during the initial years of the policy. This charge covers the costs associated with issuing the policy, such as agent commissions and administrative expenses.

Impact: Reduces the amount invested in the market-linked funds, potentially impacting your long-term returns.

2. Mortality Charges:

What it is: These charges cover the insurance risk associated with the policy. They are deducted from your fund value to cover the potential payout in case of the policyholder's death.

Impact: Can impact your returns, especially in the initial years of the policy.

3. Fund Management Charges:

What it is: These charges are levied by the insurance company to manage the investment funds within the ULIP. They cover the costs of research, investment decisions, and fund administration.

Impact: Deducted from the fund value, impacting your overall returns.

4. Policy Administration Charges:

What it is: These charges cover the administrative costs associated with managing the policy, such as record-keeping and customer service.

Impact: A small deduction from your fund value, but can add up over time.

5. Fund Switching Charges:

What it is: If you switch between different funds within the ULIP, you may be charged a switching fee.

Impact: Can impact your returns if you frequently switch between funds.

6. Partial Withdrawal Charges:

What it is: If you make partial withdrawals from your ULIP before the lock-in period, you may be charged a withdrawal fee.

Impact: Can reduce the amount you receive from your partial withdrawal.

7. Policy Surrender/Discontinuance Charges:

What it is: If you surrender or discontinue your ULIP before the lock-in period, you may be charged a surrender/discontinuance fee.

Impact: Can significantly impact your returns and may result in a loss of investment.

8. Rider Charges:

What it is: If you add any riders to your ULIP, such as accidental death benefit or critical illness cover, you will be charged an additional premium for the rider.

Impact: Increases your overall premium cost.

9. Goods and Services Tax (GST):

What it is: GST is applicable on most of the charges associated with ULIPs.

Impact: Increases the overall cost of the policy.

Important Considerations:

IRDAI Regulations: The Insurance Regulatory and Development Authority of India (IRDAI) has set limits on the charges that insurance companies can impose on ULIPs.

Charge Disclosure: Ensure you carefully review the product brochure and statement of additional information (SAI) to understand the specific charges applicable to your ULIP.

Long-Term Perspective: ULIPs are long-term investment products. It's essential to consider the impact of charges over the long term and their potential impact on your overall returns.

Cover and Save

Your partner in financial security and growth. We are registered insurance agent under License No-01632832 with HDFC life

Contact us

Advice

naveenkumar@coverandsave.com |saiteja@coverandsave.com

+917981002025

© 2025. All rights reserved.